On June 26, the Federal Reserve (FED) released the results of the stress test conducted for 31 banks. This year, 9 more banks were tested compared to last year because, according to regulatory standards, banks with assets between $100 billion and $250 billion must undergo the test every other year.

What is the FED stress test?

The FED implemented this test after the 2007-2009 financial crisis to ensure that banks can withstand a similar shock in the future. Through this test, the FED aims to determine how banks would perform under a hypothetical severe economic crisis scenario by projecting losses, revenues, expenses, and capital levels. Thus, they verify that banks have enough capital to absorb losses and continue operating during crises.

The severely adverse scenario for this year included a severe global recession, a 40% drop in commercial real estate prices, a 36% decline in housing prices, an unemployment rate peaking at 10%, and a decrease in economic output.

Stress test results

The results show that the participating banks would have enough capital to collectively absorb $685 billion in losses and continue lending under adverse conditions. While this would indicate a larger decline in capital compared to last year's scenario, it still falls within the range of the most recent tests.

Furthermore, the CET1 ratio - a measure of financial strength and high-quality capital - would drop to 9.9%, its lowest level in the past five years, although still well above the minimum requirement of 4.5%. The Fed concludes that the larger decline in the ratio can be attributed to three main factors: the increase in credit card delinquencies, riskier corporate loan portfolios, and higher expenses together with reduced commission income.

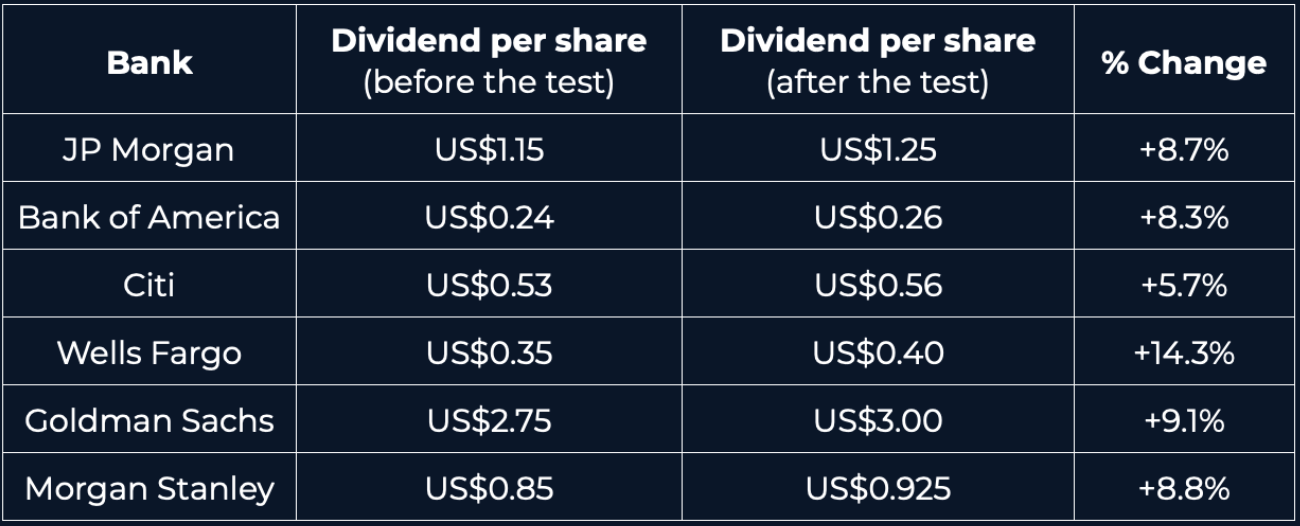

Impact on the capital market

The banks decided to increase their upcoming dividends and repurchase shares after passing the test, demonstrating that they have sufficient capital reserves.

Days after the test, JP Morgan and Morgan Stanley announced share buyback programs of $30 billion and $20 billion, respectively.

On the other hand, other participating banks decided to increase their dividends for the third quarter of 2024.

At Numa, we actively monitor the market to identify potential investment opportunities for the benefit of our clients.