In a climate marked by trade and geopolitical tensions during the early months of the year, the S&P 500 and Nasdaq Composite indices reached their lowest levels on April 8. From that point forward, they began an upward trajectory, ultimately hitting record highs in the first weeks of July. According to J.P. Morgan, this represented a rapid and unprecedented recovery.

Key Drivers of the Recovery

- Progress in Trade Negotiations: The United States reduced trade frictions through partial agreements with strategic partners. These included expanded tariff benefits with the European Union, lowered technology tariffs with China, and a suspension of agricultural tariffs with the United Kingdom—creating a more stable and predictable global trade environment.

- Easing Inflationary Pressures: Inflation in the U.S. showed clear signs of deceleration, which eased market concerns about further aggressive interest rate hikes by the Federal Reserve.

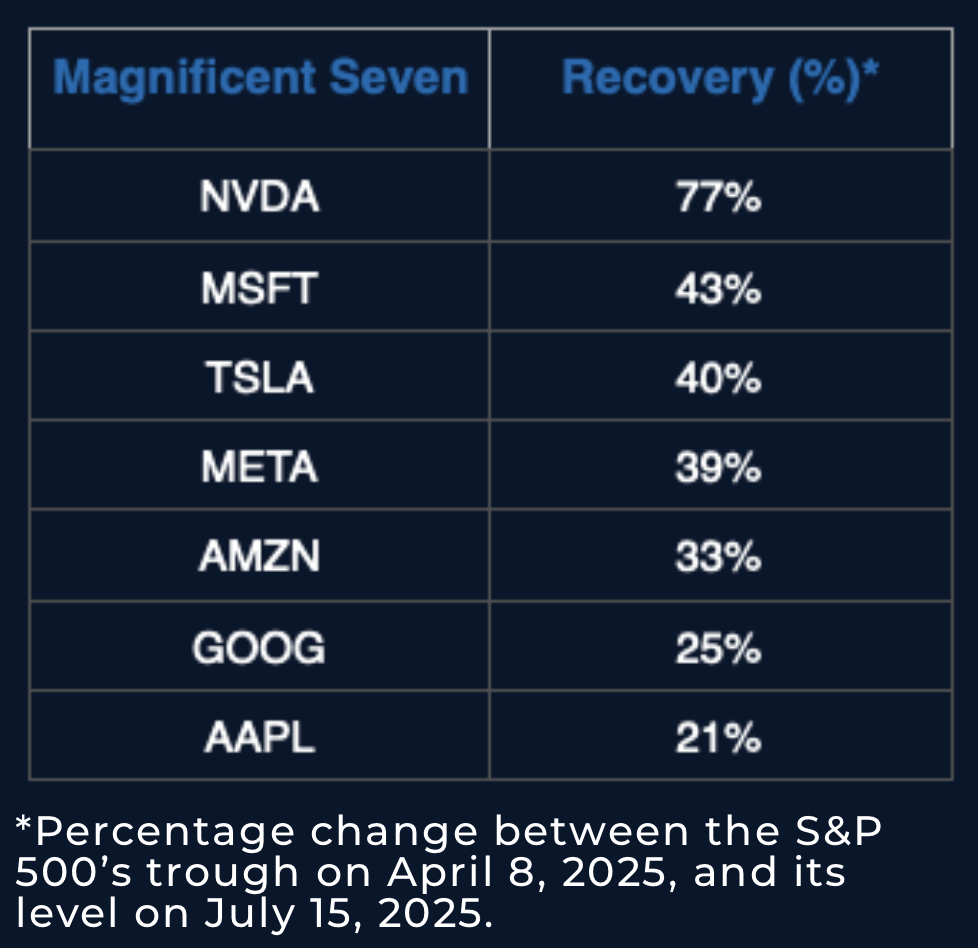

- Strong Performance in the Technology Sector: The “Magnificent Seven” (Apple, Microsoft, Alphabet, Amazon, Meta, NVIDIA, and Tesla) reported strong financial results, fueled by the growth of artificial intelligence. Their performance had a significant positive impact on equity indices, where these firms represent a substantial share of the market capitalization.

Market Outlook

Markets have interpreted the first-quarter volatility as transitory and are now signaling a more optimistic view of economic indicators. In light of this, Goldman Sachs, J.P. Morgan, and Bank of America have raised their year-end 2025 targets for the S&P 500. Additionally, the Federal Reserve is expected to begin a gradual rate-cutting cycle in the near term, further enhancing the appeal of equities.

-

Miami: 1200 Brickell Ave . No. 1950 Miami,

FL 33130.

Miami: 1200 Brickell Ave . No. 1950 Miami,

FL 33130.

-

New York: 14 Wall St. 20th Floor, New York City, NY, 10005